代码拉取完成,页面将自动刷新

![]()

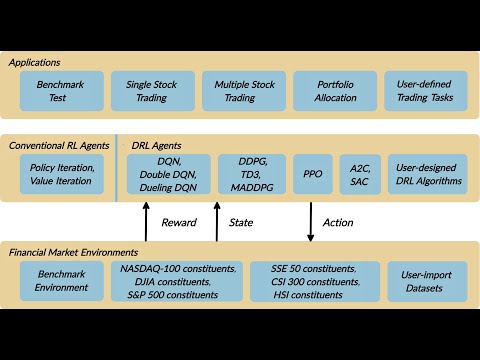

FinRL is an open source framework to help practitioners pipeline the development of trading strategies. In deep reinforcement learning (DRL), an agent learns by continuously interacting with an environment, in a trial-and-error manner, making sequential decisions under uncertainty and achieving a balance between exploration and exploitation. The open source community AI4Finance (to efficiently automate trading) provides resources about deep reinforcement learning (DRL) in quantitative finance, and aim to accelerate the paradigm shift from conventional machine learning approach to RLOps in finance.

To contribute? Please check the end of this page.

Feel free to report bugs via Github issues, join the mailing list: AI4Finance, and discuss FinRL in slack channel:

Roadmaps of FinRL:

FinRL 1.0: entry-level toturials for beginners, with a demonstrative and educational purpose.

FinRL 2.0: intermediate-level framework for full-stack developers and professionals. Check out ElegantRL

FinRL provides a unified machine learning framework for various markets, SOTA DRL algorithms, benchmark finance tasks (portfolio allocation, cryptocurrency trading, high-frequency trading), live trading, etc.

We published papers in FinTech and now arrive at this project:

A YouTube video about FinRL library. [YouTube] AI4Finance Channel for quant finance.

We implemented Deep Q Learning (DQN), Double DQN, DDPG, A2C, SAC, PPO, TD3, GAE, MADDPG, MuZero, etc. using PyTorch and OpenAI Gym.

# grant access to execute scripting (read it, it's harmless)

$ sudo chmod -R 777 docker/bin

# build the container!

$ ./docker/bin/build_container.sh

# start notebook on port 8887!

$ ./docker/bin/start_notebook.sh

# proceed to party!

Build the container:

$ docker build -f docker/Dockerfile -t finrl docker/

Start the container:

$ docker run -it --rm -v ${PWD}:/home -p 8888:8888 finrl

Note: The default container run starts jupyter lab in the root directory, allowing you to run scripts, notebooks, etc.

Clone this repository:

git clone https://github.com/AI4Finance-LLC/FinRL-Library.git

Install the unstable development version of FinRL:

pip install git+https://github.com/AI4Finance-LLC/FinRL-Library.git

For OpenAI Baselines, you'll need system packages CMake, OpenMPI and zlib. Those can be installed as follows:

sudo apt-get update && sudo apt-get install cmake libopenmpi-dev python3-dev zlib1g-dev libgl1-mesa-glx

Installation of system packages on Mac requires Homebrew. With Homebrew installed, run the following:

brew install cmake openmpi

To install stable-baselines on Windows, please look at the documentation.

cd into this repository:

cd FinRL-Library

Under folder /FinRL-Library, create a Python virtual-environment:

pip install virtualenv

Virtualenvs are essentially folders that have copies of python executable and all python packages.

Virtualenvs can also avoid packages conflicts.

Create a virtualenv venv under folder /FinRL-Library

virtualenv -p python3 venv

To activate a virtualenv:

source venv/bin/activate

To activate a virtualenv on windows:

venv\Scripts\activate

The script has been tested running under Python >= 3.6.0, with the following packages installed:

pip install -r requirements.txt

Stable-Baselines3 is a set of improved implementations of reinforcement learning algorithms in PyTorch. It is the next major version of Stable Baselines. If you have questions regarding Stable-baselines package, please refer to Stable-baselines3 installation guide. Install the Stable Baselines package using pip:

pip install stable-baselines3[extra]

A migration guide from SB2 to SB3 can be found in the documentation.

Still Under Development

python main.py --mode=train

Use Quantopian's pyfolio package to do the backtesting.

The stock data we use is pulled from Yahoo Finance API.

(The following time line is used in the paper; users can update to new time windows.)

@article{finrl2020,

author = {Liu, Xiao-Yang and Yang, Hongyang and Chen, Qian and Zhang, Runjia and Yang, Liuqing and Xiao, Bowen and Wang, Christina Dan},

journal = {Deep RL Workshop, NeurIPS 2020},

title = {FinRL: A Deep Reinforcement Learning Library for Automated Stock Trading in Quantitative Finance},

url = {https://arxiv.org/pdf/2011.09607.pdf},

year = {2020}

}

Will maintain FinRL with the "AI4Finance" community and welcome your contributions!

Please check the contributing guidances.

Thanks to all the people who contribute.

Support more markets, so that the users can test their stategies.

Maintain a pool of DRL algorithms that can be treated as SOTA implementations.

To help quants have better evaluations, will maintain benchmarks for many trading tasks, upon which you can improve for your own tasks.

Supporting live trading can close the simulation-reality gap, it will enable quants to switch to the real market when they are confident with their strategies.

MIT

此处可能存在不合适展示的内容,页面不予展示。您可通过相关编辑功能自查并修改。

如您确认内容无涉及 不当用语 / 纯广告导流 / 暴力 / 低俗色情 / 侵权 / 盗版 / 虚假 / 无价值内容或违法国家有关法律法规的内容,可点击提交进行申诉,我们将尽快为您处理。